Why Keynesian Economics Is Collapsing

When Economic Theory Stops Working

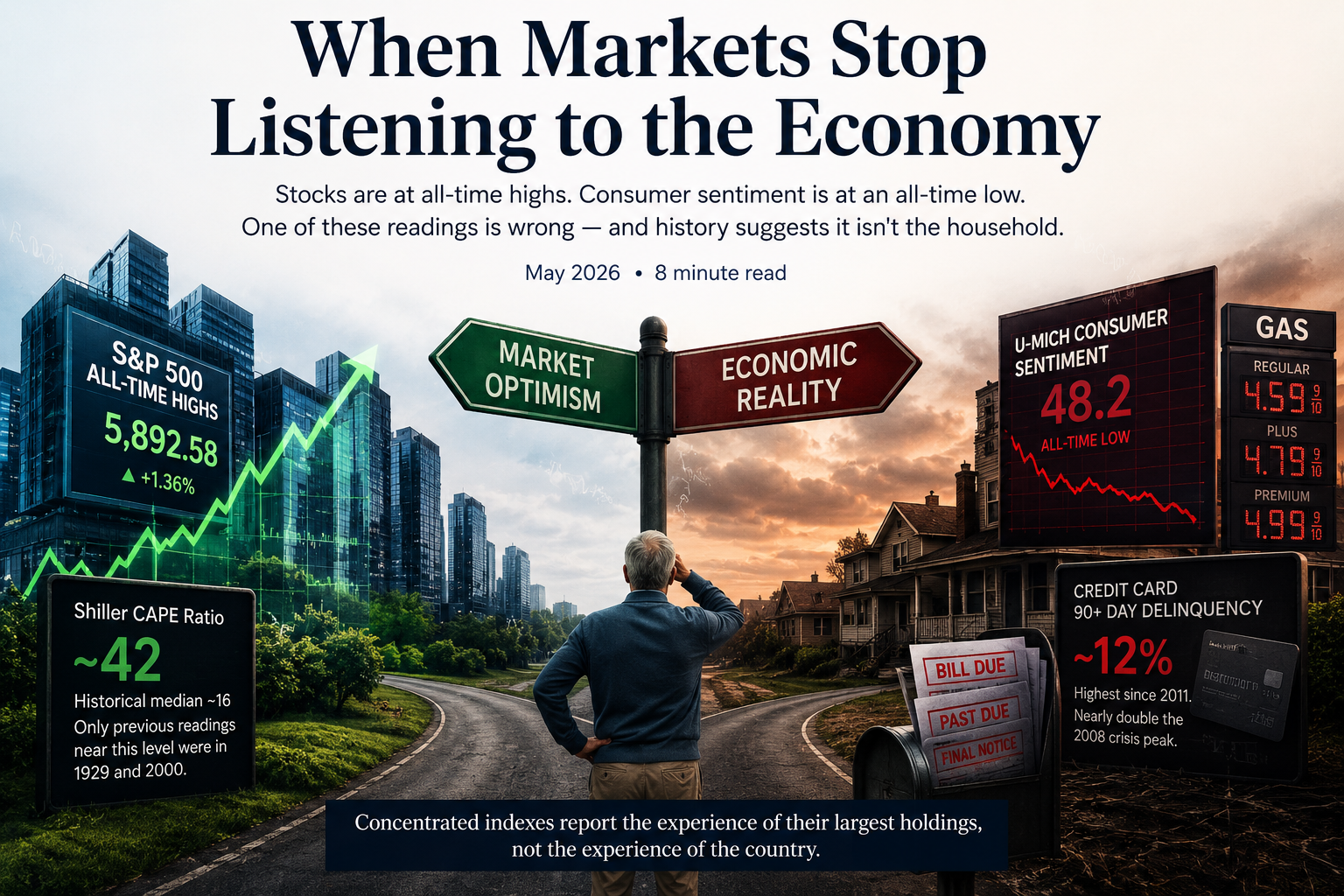

For decades, investors have relied—often unknowingly—on a single assumption: when economic stress appears, policymakers will step in and restore balance. That assumption comes from Keynesian economics, the framework developed by John Maynard Keynes in the 1930s. It shaped how governments spend, how central banks intervene, and how portfolios are built.

Today, that framework is breaking down.

The Conditions Keynes Assumed No Longer Exist

Keynesian policy was designed for a world with limited government debt, temporary deficits, and intact public confidence. Government intervention was meant to be counter-cyclical, not permanent. Those guardrails are gone.

Debt is now structural, not cyclical. Deficits no longer shrink in expansions. Central banks are constrained by the fiscal consequences of their own policies. And confidence—arguably the most important variable of all—has weakened.

When confidence erodes, stimulus loses effectiveness.

Why Policy Is Producing Diminishing Returns

Raising rates no longer reliably slows demand—it increases government interest expense. Lowering rates no longer stimulates productive investment—it inflates asset prices. Quantitative easing has distorted markets without restoring organic growth.

In short, the tools still exist, but they no longer work the way they once did.

What Markets Are Signaling

Markets adapt before they break. The signals are subtle but persistent:

Asset prices rising without corresponding economic strength

Volatility appearing suddenly, not gradually

Policy announcements moving markets less than they used to

Capital favoring scarcity and durability over leverage

These are not signs of stability. They are signs of a system under strain.

Why Traditional Portfolio Assumptions Are at Risk

Buy-and-hold strategies were built for an era when cycles resolved, policy restored balance, and time healed most drawdowns. In a world of permanent intervention and rising debt, cycles stretch, recoveries weaken, and correlations rise.

Risk is not gone—it is merely hidden.

A Quiet Shift in Investor Behavior

As confidence in policy frameworks fades, investors naturally migrate toward assets that do not depend on political discipline or economic theory working as intended. This explains the renewed interest in real assets, capital preservation, and resilience-based strategies.

This shift is not emotional. It is structural.

The Takeaway

The collapse of Keynesian economics does not mean markets are ending. It means the assumptions behind decades of policy-driven stability no longer hold.

Portfolios built for “normal times” deserve to be re-examined.

History does not repeat—but it does change the rules.

And when the rules change, risk management matters more than optimism.